Q4 2024 Quarterly Compass Economic Update

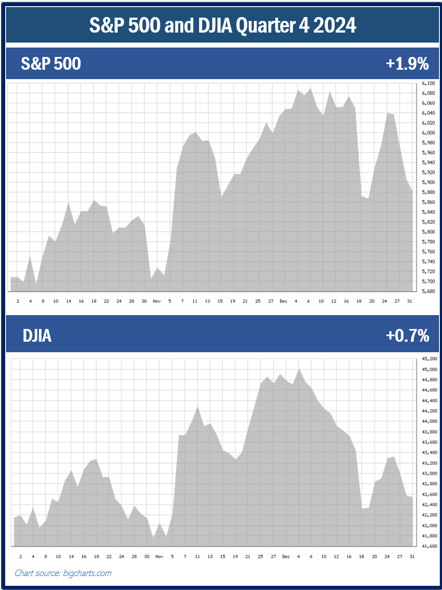

2024 was another strong year for equity investors. While not as good as the year’s first three quarters, the fourth quarter still finished with positive returns, more record highs, and an optimistic outlook toward 2025. Historically, equities have advanced in the fourth quarter and after a series of ups and downs, they finished ahead of where they started.

Equity markets entered the quarter with strong momentum and after the election results in early November, they responded favorably. They were also helped during the quarter by continued monetary easing from the Federal Open Market Committee (FOMC).

The S&P 500 index ended 2024 with nearly the same results as 2023. For 2024, the S&P 500 closed the year with a gain of more than 23% (24.23% in 2023) and had 57 record closes. The Dow Jones Industrial Average (DJIA) ended the year up almost 13% (13.7% in 2023). (www.macrotrends.net; cnbc.com 1/2/25)

The S&P 500 entered the fourth quarter with impressive annual returns but stumbled to the finish line and produced the year’s lowest quarterly return of approximately 2.0%. The DJIA was up less than 1% during the fourth quarter. (cnbc.com 1/2/25) The Fed reduced interest rates three times in 2024. During the fourth quarter, the Fed implemented two interest rate drops, one in December , thus concluding the year with three interest rate cuts in a row.

After the December FOMC meeting, the Federal Reserve released a statement, noting, “Recent indicators suggest that economic activity has continued to expand at a solid pace. Since earlier in the year, labor market conditions have eased and the unemployment rate has moved up but remains low. Inflation has made progress toward the Committee’s 2 percent objective but remains slightly elevated.” As a result of this data, the Fed felt it appropriate to make a third and final rate cut for 2024.

In November, the unemployment rate was 4.2%, and wage growth increased by 0.4%. The data from these two key economic indicators is closely monitored by the Federal Open Market Committee (FOMC) to help inform the Fed when making monetary policy decisions.

While some analysts are optimistic, many are citing that the upcoming year will bring new and long-standing issues that could affect the U.S. economy. A new administration with proposed policy changes, monetary easing, and continued geo-political unrest are just a few matters that will bring uncertainty to equity markets.

New administration: Elected President Trump has promised to bring changes when he returns to the Oval Office. How these changes will affect the U.S. and global economies is yet to be seen.

Monetary policy changes: While the Fed did reduce interest rates in 2024, their outlook for 2025 was more hawkish as of December. The Fed has a goal of 2% inflation and maximum employment. In the FOMC statement in December, it stated, “The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.”

Continued geo-political unrest: The Russia-Ukraine war continues, and conflict in the Middle East remains. In addition, proposed tariffs on imports from foreign countries could directly affect equities and the U.S. economy.

As your financial professionals, we are committed to keeping you aware of any changes and activities that could directly affect your unique situation. Our goal is to continuously review our client’s investments and confirm they align with their time horizon, risk tolerance and goals.

Inflation & Interest Rates

Key Points:

- Interest rates were reduced by the Fed two times during the fourth quarter.

- Further Fed rate cuts are anticipated in 2025. At their September meeting, four future reductions were mentioned; however, at the December FOMC meeting, that number was reduced to two.

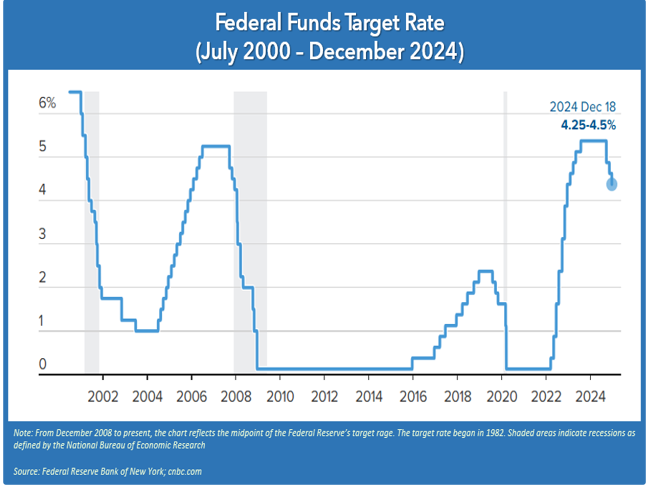

Federal Funds interest rates started 2024 at a range of 5.25% to 5.5%. During the last four months of the year, the Federal Reserve began a campaign to ease monetary policy and lower interest rates. They started in September with a rate reduction of 50 basis points. At the November Federal Open Market Committee (FOMC) meeting, interest rates were reduced by another 25 basis points, bringing the benchmark range down to 4.5% to 4.75%. At the December meeting, the Fed ended 2024 with another 25-basis point reduction, finishing the year with Federal Funds rates at 4.25% to 4.5%. Equities responded favorably to the first two rate cuts, but in December, they took a tumble due to the Fed’s forecast which significantly pared-back interest rate cuts in 2025. At the September FOMC meeting, they originally expected four rate cuts in 2025. At the December meeting, this forecast was cut in half. As of December, the Fed is now forecasting rates to be reduced by 0.50% in 2025.

December’s reduction marked the third interest rate cut of the year after 11 increases made between March 2022 and July 2023.

The Fed was encouraged to ease its policy due to key indicators that suggested, “economic activity continued to expand at a solid pace”, as stated in the FOMC press release following the adjournment of the November 7 meeting. Inflation was gradually moving closer to the Fed’s 2% target, labor market conditions were easing, and the unemployment rate remained low.

Uncertainty about interest rates persists as we move into 2025. The Federal Reserve is committed to their mandate to maintain strong employment rates while striving to return inflation to its target of 2%. They will continue to monitor key indicators to determine their approach to interest rates and are prepared to adjust their monetary policy stance if necessary. According to the FOMC’s press release in November, “The Committee’s assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and expectations, and financial and international developments.”

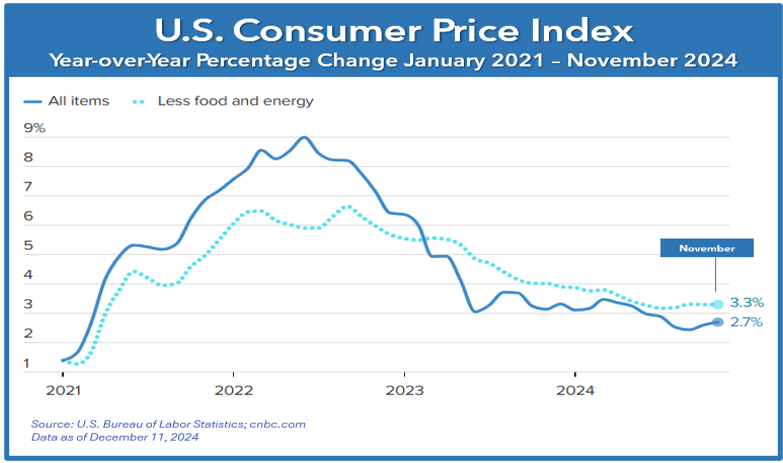

In November, the Consumer Price Index (CPI) recorded its largest increase in seven months, rising by 0.3%. The core CPI, which excludes food and energy prices and is often viewed by economists as a better gauge of future inflation, also increased by 0.3%.

A 0.3% rise in shelter costs accounted for nearly 40% of the overall increase. Hotel prices spiked by 3.7%, impacting vacationers. Additionally, food prices rose by 0.4%, with groceries increasing by 0.5%. A significant factor contributing to this food price rise was the recent avian flu outbreak, which resulted in an 8.2% increase in egg costs in November.

As of the November FOMC meeting, the median Fed staff forecast calls for a rate range of 3.75%-4.00% by the end of 2025.

Interest and inflation rate movements are integral to investors’ financial planning, so we will continue to monitor these key economic indicators.

The Bond Market and Treasury Yields

Key Points:

- Outlooks for bonds in 2025 are hazy. If interest rates continue to fall, bonds should appreciate. However, if inflation does an about-face due to potential policy changes, interest rates might stagnate or rise.

- Current bond yields could present an appealing option for investors seeking more stability against market volatility.

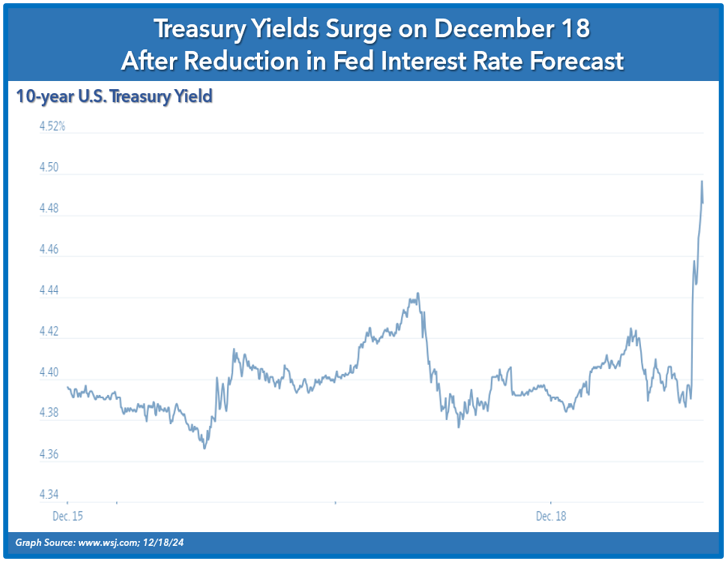

Bonds have an inverse relationship with interest rates—when one goes up, the other usually goes down. After December’s Federal Open Market Committee meeting, treasury yields rose due to the news that fewer rate cuts were anticipated for 2025. This shift in outlook prompted investors to prefer longer-term treasuries and triggered a wave of selling mid-term U.S. Treasurys, driving some bond prices lower and yields higher. The two-year yield dropped to 4.295%, while the 10-year rose to 4.56%, and was trading around its highest level since late May. That yield variance left the two-year trading around 0.26 percentage points below the 10-year. This is a level that has not been seen since June 2022.

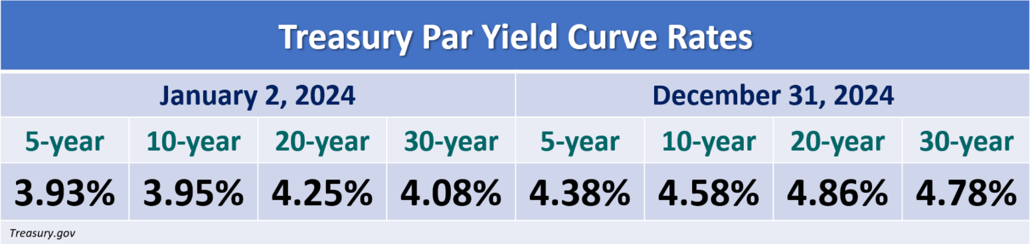

On December 31, the 10-year note was 4.58%, higher than at the end of the third quarter, when it reached 3.81%. The 20-year treasury ended the fourth quarter at 4.86% and the 30-year note closed at 4.78% (Source: treasury.gov)

Yields rose at the end of 2024 and are currently close to multi-decade highs, even with interest rates forecasted to continue falling in 2025. If everything unfolds as expected, this could make bonds, which historically have lower volatility than stocks, a more appealing option as a stable alternative to cash, as well as a hedge against market volatility. On the contrary, interest rates could stagnate if inflation remains belligerent or even reaccelerates.

Bonds can be a part of a well-diversified portfolio and we consider using them for clients based on each client’s unique situation. Please remember that while diversification in your portfolio can help you pursue your goals, it does not ensure a profit or guarantee against loss.

Investor’s Outlook

Key Points:

- Investors enter 2025 with a mix of optimism, anticipation and caution.

- Investors have enjoyed strong annual returns in 2023 and 2024: both up over 20%, compared with the long-run average of about 10%.

- Equities have historically been good long-term investments and one of the best exercises for investors is to revisit their time horizons.

Looking ahead to 2025, investor sentiment remains hopeful and there is a mix of optimism, anticipation and caution. Despite moments of wavering, the U.S. economy has experienced impressive growth, and many believe the current bull market will continue. Key factors such as low unemployment rates, slowing inflation, strong corporate earnings, monetary easing, investor enthusiasm for Artificial Intelligence (AI), and significant market returns have kept investor confidence high. Fears of a recession, while still around, have reduced, as the Federal Reserve continues to fight inflation without slowing down economic growth.

The past few years have been exceptional for the U.S. stock market. Moving into 2025 a major question is the US economy and economic growth. The new year will bring changes that could potentially increase volatility. There should be adjustments to policy and tax laws. Additionally, the possibility of new tariffs and their impact on inflation and the equity markets needs to be monitored.

While inflation is relatively moderate compared to previous years, it is still above the Fed’s target of 2%. Although the Fed reduced interest rates three times in a row at the end of 2024, the persistent nature of inflation and certain proposed economic policies may lead them to slow or pause easing efforts in 2025. Federal officials closely monitor key indicators such as housing, labor markets, and

core goods to advise their decisions regarding monetary policy. While the Fed expects to implement more rate cuts in 2025, recent years have taught us to remain vigilant and prepared for unexpected circumstances.

Analysts have mixed outlooks for the markets in 2025. Many are optimistic about a continued market rally driven by ongoing AI growth and deregulation, as well as the potential for lower taxes. If interest rates keep going down, this could fuel the stock market forward. However, on the other end, some are concerned that equities are highly priced and could see some setbacks.

Investors have enjoyed strong annual returns in 2023 and 2024: both up over 20%, compared with the long-run average of about 10%. History teaches us that after that kind of run you need to be prepared for a possible pullback. Also, valuations of some leading equities are historically high, which is another indicator that it could be more likely that equities experience a pullback sometime during 2025. Having said that, momentum is also high and long-term investors never want to be caught trying to time equity markets.

When the S &P index falls more than 10% from a recent high, it is said to have entered “correction” territory. There have been 24 market corrections since November 1974. They historically happen on average about every 18 months. The S&P 500 did not experience a correction in 2024.

Analysts say that corrections are healthy and even necessary for bull markets. They help shake out some of the so-called froth in the stock market, where prices run up too dramatically and get ahead of themselves. Analysts also share that a correction isn’t necessarily something to dread. Most strategists are still predicting solid earnings growth for equities in 2025. With that backdrop, stocks could head higher, even if there are some bumps in the road.

So, what should investors do?

One of the best exercises for investors is to revisit their time horizons. Equities are mainly long-term investments and investors should be prepared to hold equity positions for at least five years or more. The goal is to potentially allow enough time to recoup any downfalls that occur. A well-disciplined plan incorporates the fact that equities do not move in a straight line and the benchmark for investment returns is long-term. The term “correction” is used for downturns of 10% to 20% because historically the market drop often “corrects” and returns equity prices to their longer-term trend.

The American Association of Individual Investors (AAII) surveyed investors in December and reported that 43% of respondents were bullish about the stock market over the coming six months, 32% were bearish, and 25% felt neutral. (Source: www.fool.com; 12/20/24)

As we head into the new year, we will continue to monitor inflation, interest rates, key economic data, and monetary policy changes. It is obvious that changes are on the horizon, which brings uncertainty and the potential for increased market volatility. Regardless of what happens moving forward, we will uphold our mantra of “proceed with caution.”

It is important to resist the emotional temptation to deviate from your long-term strategy. Many times, it can be tempting to “cash out while the going is good,” but doing so could result in missing out on additional gains. While we can all analyze, speculate and theorize, trying to predict short-term market movements is always challenging and difficult; therefore, we prefer to rely on a well-planned, long-term strategy that considers market volatility, your time horizon, and risk tolerance. Such a strategy should serve as a benchmark for savvy investors. As always, you should stay informed about the news but minimize your exposure to avoid getting caught up in speculative claims, unfounded predictions and fearmongering.

We believe in proactive preparation, and our aim is to provide our clients with a solid financial strategy that is thoughtfully designed for all market environments. Rebalancing and appropriate diversification are important for all our clients. If you would like us to look at your financial situation, please contact us.

Our goal in 2025 is to exceed your expectations. We take pride in offering a high-level service that includes consistent and meaningful communication throughout the year. We always recommend discussing any changes, concerns, or ideas you may have with us before making any financial decisions. This way, we can help you determine the best strategy for your situation. Keep in mind that there are often other factors to consider when altering anything in your financial plan, such as tax implications, increased risk, and changes in your time horizon.

We value our clients and are accessible to them. If you would like to explore our services, feel free to contact us with any concerns or questions you may have.

team@stablerwm.com | (425) 646-6327

Securities and financial planning services provided through LPL Financial, a Registered Investment Advisor. Member FINRA/SIPC.

Note: The views stated in this letter are not necessarily the opinion of broker/dealer, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward-looking statements and projections. There are no guarantees that these results will be achieved. All indices referenced are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

The S&P 500 is an unmanaged index of 500 widely held stocks that is general considered representative of the U.S. Stock market. The modern design of the S&P 500 stock index was first launched in 1957. Performance prior to 1957 incorporates the performance of the predecessor index, the S&P 90. Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stocks of companies maintained and reviewed by the editors of the Wall Street Journal. Past performance is no guarantee of future results. CDs are FDIC Insured and offer a fixed rate of return if held to maturity. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed.

There is an inverse relationship between interest rate movements and bond prices. Generally, when interest rates rise, bond prices fall and when interest rates fall, bond prices generally rise. There is no guarantee that a diversified portfolio will enhance overall returns out outperform a non-diversified portfolio. Diversification does not protect against market risk.

This content was prepared by APFA (Academy of Preferred Financial Advisors). Sources: www.cnbc.com; www.federalreserve.com; www.tradingeconomics.com; www.bankrate.com; www.forbes.com; www.nerdwallet.com; Investopedia.com; www.morningstar.com; www.bigcharts.com

Category

Stay Informed

Join our mailing list to receive monthly newsletters with information that impacts your financial decisions.

Certified Financial Planner

In Business 35+ Years