Case Study: How Jordan Maximized His Microsoft Retirement Savings Strategy

At our firm, we don’t just plan for the future; we actively shape it. This series of real-life case studies demonstrates how strategic financial planning can accelerate Microsoft professionals’ paths toward work optionality. In this edition, we highlight how we are assisting Jordan in developing a retirement savings strategy, setting him on the path to semi-retire at the age of 55.

Background:

Jordan, a 53-year-old Microsoft employee, is on a path to semi-retirement. He aims to transition to a part-time consulting role outside of Microsoft when he reaches 55. Having been with Microsoft for more than 15 years, reaching this age allows his remaining stock awards to continue vesting after separation. This crucial home stretch led us to create a detailed retirement savings game plan to maximize Jordan’s benefits and tax efficiency.

Retirement Savings Tactics:

1. Maximized 401(k) Contributions:

Jordan is planning to contribute the maximum allowable amount of $30,500 to his 401(k) in 2024, which includes a $7,500 catch-up contribution. This strategic move will secure the full 50% match from Microsoft, adding an estimated $11,250 to his retirement funds and capitalizing on substantial tax savings.

2. Health Savings Account (HSA) Utilization:

Under the Microsoft Health Savings Plan, Jordan and his wife Susan are on track to maximize their HSA contributions by adding $5,800, complemented by an additional $2,500 from Microsoft. This account provides a triple tax advantage.

3. Mega Backdoor Roth IRA Contributions

Jordan plans to use the after-tax option to add another $34,500 to his 401(k), which will be immediately converted to a Roth IRA for tax-free growth. To fund this full amount, he plans to sell some of his Microsoft stock, carefully managing tax implications.

4. Employee Stock Purchase Plan (ESPP)

Jordan is contributing the maximum $15,000 to Microsoft’s ESPP to take advantage of the 10% stock purchase discount. With the immediate return on investment, this is our preferred place to hold Microsoft stock.

5. Backdoor Roth IRA:

With no pre-existing traditional IRAs, both Jordan and Susan contributed $8,000 each to their Roth IRAs using the backdoor method, further enhancing their portfolios with tax-free growth potential.

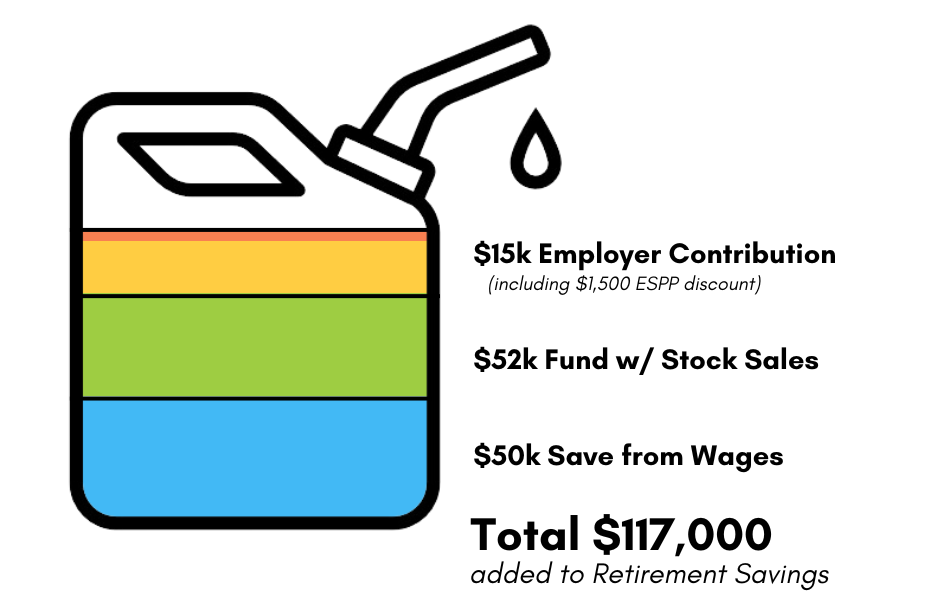

Results and Future Planning

By the end of 2024, Jordan’s total savings contributions are projected to amount to over $100,000! Microsoft will contribute an additional +$15,000 (including the ESPP discount), totaling more than $115,000 added to Jordan’s retirement savings at a tax advantage or discount benefit.

Over the years, Jordan has accumulated over $1 million in Microsoft stock, which represents an overconcentration and poses a retirement risk. This year, he intends to strategically sell shares of this over-concentrated stock, to help fund these retirement contributions.

Conclusion: Tailored Strategies for Financial Success

Jordan’s proactive approach is a prime example of how customized financial planning can significantly enhance retirement outcomes. Recognizing that each Microsoft employee’s financial situation is unique, we offer personalized consultations to help identify and implement the most effective strategies for your circumstances.

Don’t wait to secure your financial future! Schedule a strategy session with our team today to explore how you can start crafting your own financial success story.

Contact Us:

team@stablerwm.com | (425) 646-6327

No strategy assures success or protects against loss. Stabler Wealth Management and LPL Financial are not affiliated or endorsed by Microsoft.

This is a hypothetical situation based on real life examples. Names and circumstances have been changed. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investments or strategies may be appropriate for you, consult your advisor prior to investing.

This is a hypothetical example and is not representative of any specific investment. Your results may vary.

Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA.

Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax in addition to current income tax.

Securities and financial planning services provided through LPL Financial, a Registered Investment Advisor. Member FINRA/SIPC.

Category

Stay Informed

Join our mailing list to receive monthly newsletters with information that impacts your financial decisions.

Certified Financial Planner

In Business 35+ Years